In the world of affordable housing finance, the 50% test has long been the gatekeeper for 4% Low-Income Housing Tax Credits (LIHTCs). Developers had to finance at least half of a project’s aggregate basis with tax-exempt bonds to qualify. That changed with the signing of the Big Beautiful Bill—and if we manage it well, it’s a change that could reshape California’s housing landscape.

Starting with projects placed in service after December 31, 2025, the threshold drops to 25%. California’s Tax Credit Allocation Committee (CTCAC) and Debt Limit Allocation Committee (CDLAC) have already adopted emergency regulations to implement this shift. For a state facing a severe housing shortage and a tight bond cap, this is big news.

So, why does this matter and what’s the history of the 50% test?

The 50% test dates back to the creation of the LIHTC program in 1986. Congress designed it to ensure that projects using 4% credits were substantially financed with tax-exempt bonds, which also count against a state’s private activity bond cap. For decades, this rule worked—but as housing costs soared and bond caps tightened, the 50% requirement became a bottleneck. Developers sometimes found themselves in a position where they felt pressure to borrow more than they really needed in order to qualify for credits. The new 25% threshold is intended to ease that pressure and unlock more housing production nationwide. However, while lowering the threshold to 25% frees up bond cap and opens the door for more projects—especially those serving extremely low-income populations, there are trade-offs.

With that in mind, here are some Pros and Cons of the 25% Test

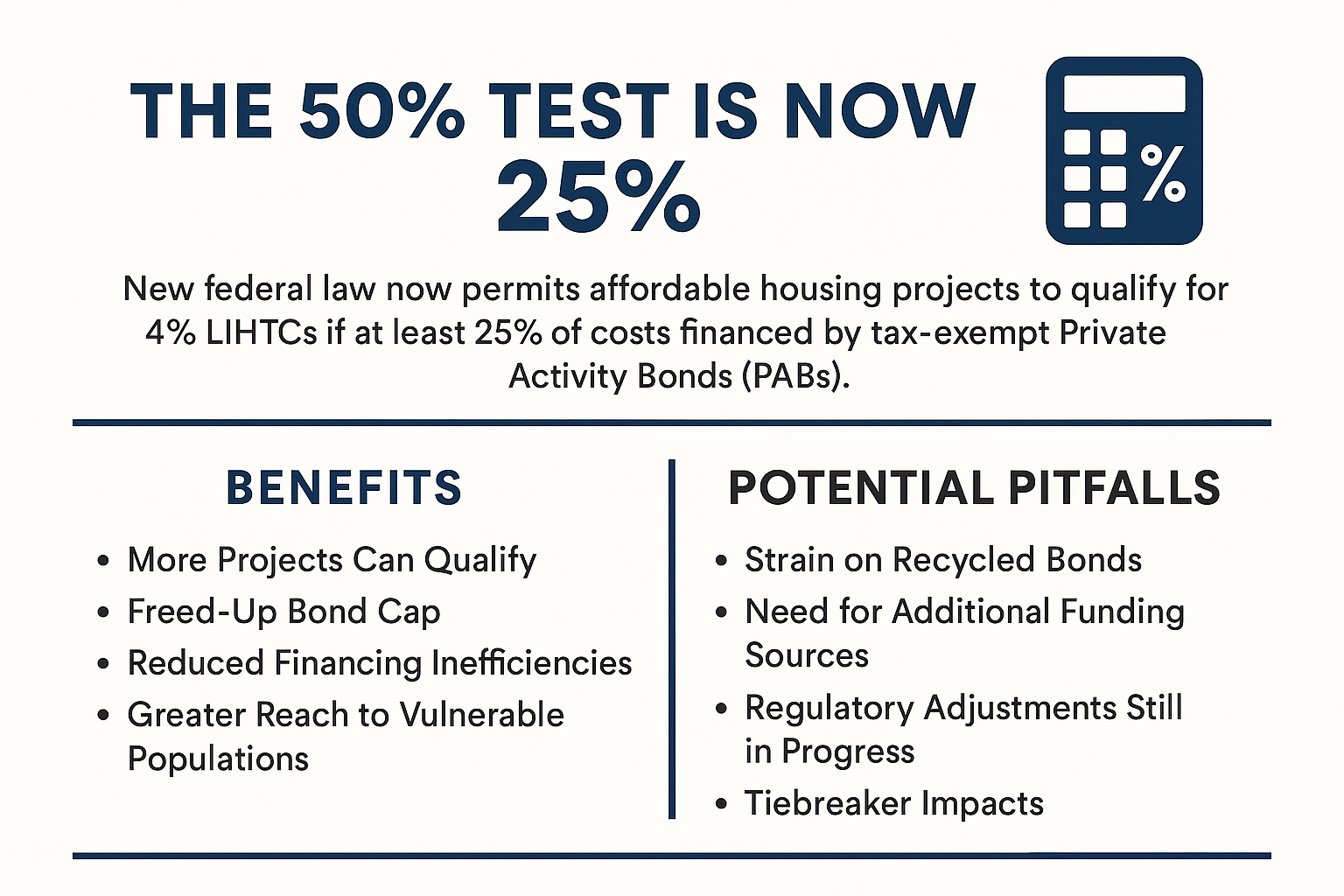

- PRO – More projects can qualify, especially those with lower rents or serving vulnerable populations.

- PRO – Frees up bond cap, allowing the same allocation to finance more developments.

- PRO – Reduces financing inefficiencies—no more costly post-construction bond refinances.

- PRO – Lower issuance costs and less long-term debt for developers.

- PRO – Greater reach for projects targeting seniors, people with disabilities, and formerly homeless individuals.

- CON – Bigger financing gaps—projects may need more soft funding or deferred fees.

- CON – Increased competition for recycled bonds to meet CDLAC scoring requirements.

- CON – There may be higher reliance on taxable debt, which comes with higher interest rates.

- CON – Regulatory adjustments still in progress—developers need to stay alert.

- CON – New underwriting challenges as financial models adapt to smaller bond allocations.

Here’s the bottom line: The 25% test is a game-changer for California. It could unlock thousands of new affordable homes, but it also requires developers to rethink their financing strategies. Flexibility and creativity will be key as will relationships with government partners, funders, and lenders.

At the California Council for Affordable Housing (CCAH), we’re advocating for policies that maximize this opportunity and make more affordable housing a reality. If you’re not yet a member, now is the time to join us. Together, we can shape the future of housing in California.